L2 (Ridge regularisation)#

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

from sklearn.linear_model import Ridge

from sklearn.preprocessing import OneHotEncoder

from IPython.display import clear_output

Souces#

https://www.statlearning.com/ chapter 6.

Description#

In L2-regularisation, a component is added to the target function of the coefficient estimation method:

Where:

\(\beta_j\) - estimated coefficient;

\(\lambda\) - parameter indicating how much the model should be regularised.

Regression#

L2-regularisation combined with a regression model is called ridge regression.

So if we use MSE as a quality function, we will have a modifide function:

Where:

\(n\) - sample size;

\(p\) - data dimention;

\(x_i = (x_{i1}, x_{i2}, ..., x_{ip})\) - vector describing the \(i\text{-}th\) observation;

\(\beta = (\beta_1, \beta_2, ..., \beta_p)\) - vector of coefficient estimates.

Note To perform refularization to regression you need to ensure that your features have the same scaling. Check more here.

Compression of coefficients#

Here I reproduce the experiment from the ISLR.

Loading Credit data.

Credit = pd.read_csv("Credit.csv", index_col = 0)

nominal_names = [

"Gender", "Student", "Married", "Ethnicity"

]

ohe = OneHotEncoder(

sparse_output = False, drop = "first"

).fit(

Credit[nominal_names]

)

Credit = pd.concat(

[

pd.DataFrame(

ohe.transform(Credit[nominal_names]),

columns = ohe.get_feature_names_out(),

index= Credit.index

),

Credit.loc[:,~Credit.columns.isin(nominal_names)]

],

axis = 1

)

X = Credit.iloc[:,:-1]

y = Credit.iloc[:, -1]

Credit.head()

| Gender_Female | Student_Yes | Married_Yes | Ethnicity_Asian | Ethnicity_Caucasian | Income | Limit | Rating | Cards | Age | Education | Balance | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| ID | ||||||||||||

| 1 | 0.0 | 0.0 | 1.0 | 0.0 | 1.0 | 14.891 | 3606 | 283 | 2 | 34 | 11 | 333 |

| 2 | 1.0 | 1.0 | 1.0 | 1.0 | 0.0 | 106.025 | 6645 | 483 | 3 | 82 | 15 | 903 |

| 3 | 0.0 | 0.0 | 0.0 | 1.0 | 0.0 | 104.593 | 7075 | 514 | 4 | 71 | 11 | 580 |

| 4 | 1.0 | 0.0 | 0.0 | 1.0 | 0.0 | 148.924 | 9504 | 681 | 3 | 36 | 11 | 964 |

| 5 | 0.0 | 0.0 | 1.0 | 0.0 | 1.0 | 55.882 | 4897 | 357 | 2 | 68 | 16 | 331 |

We will increase the regularisation parameter and take the values of the coefficients. The procedure is rather long, so it is supposed to perform the calculation and put the results in a file.

# coefs_frame = pd.DataFrame(columns = X.columns)

# stand_X = X/np.sqrt(((X - X.mean())**2).sum()/X.shape[0])

# alphas = np.arange(0, 2000, 0.01)

# int_count = len(alphas)

# for i, alpha in enumerate(alphas):

# clear_output(wait=True)

# print("{}/{}".format(i, int_count))

# coefs_frame.loc[alpha] = pd.Series(

# Ridge(alpha = alpha).fit(stand_X,y).coef_,

# index = X.columns

# )

# coefs_frame.index.name = "alpha"

# coefs_frame.to_csv("l2_regularisation_files/l2_reg_coefs.csv")

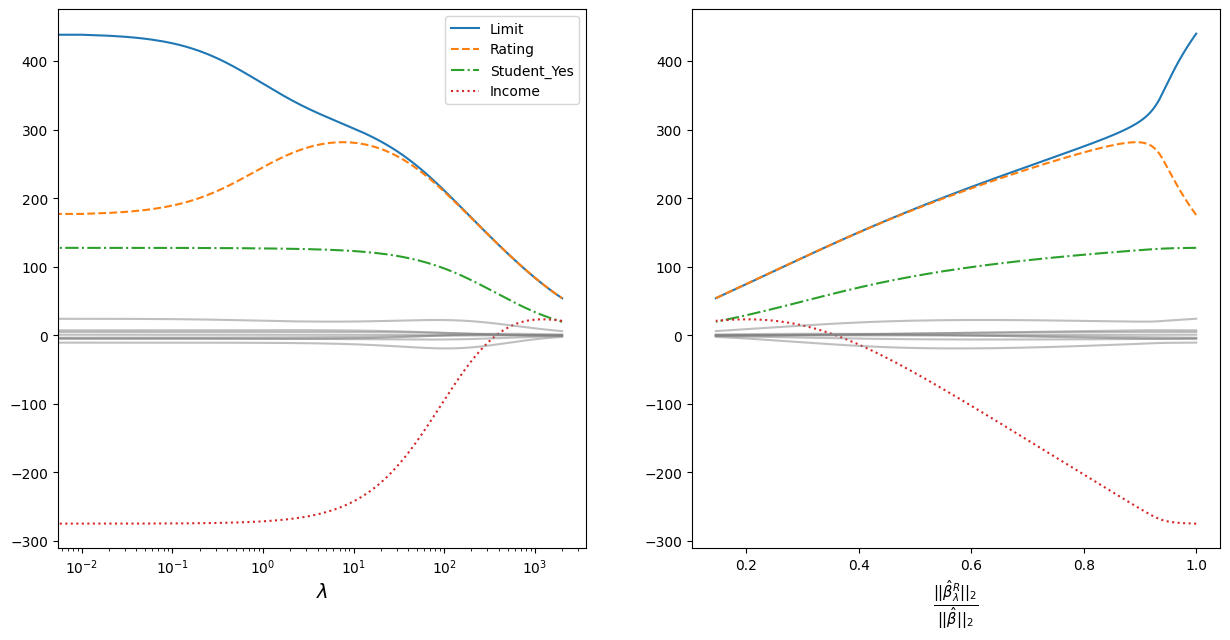

The obtained values of coefficients are plotted on the graphs.

coefs_frame = pd.read_csv("l2_regularisation_files/l2_reg_coefs.csv", index_col = 0)

plot_var_names = ["Limit", "Rating", "Student_Yes", "Income"]

line_styles = ['-', '--', '-.', ':']

beta_0 = np.sqrt(np.sum(coefs_frame.loc[0]**2))

coefs_frame["beta_i/beta_0"] = coefs_frame.apply(

lambda row: np.sqrt(np.sum(row**2))/beta_0,

axis = 1

)

plt.figure(figsize = [15, 7])

plt.subplot(121)

for i in range(len(plot_var_names)):

plt.plot(

coefs_frame.index,

coefs_frame[plot_var_names[i]],

linestyle = line_styles[i]

)

for col in coefs_frame.loc[

:, ~coefs_frame.columns.isin(plot_var_names)

]:

plt.plot(

coefs_frame.index, coefs_frame[col],

color = "gray", alpha = 0.5

)

plt.legend(plot_var_names)

plt.xlabel("$\\lambda$", fontsize = 14)

plt.gca().set_xscale("log")

plt.subplot(122)

for i in range(len(plot_var_names)):

plt.plot(

coefs_frame["beta_i/beta_0"],

coefs_frame[plot_var_names[i]],

linestyle = line_styles[i]

)

for col in coefs_frame.loc[

:, ~coefs_frame.columns.isin(plot_var_names)

]:

plt.plot(

coefs_frame["beta_i/beta_0"], coefs_frame[col],

color = "gray", alpha = 0.5

)

ans = plt.xlabel(

"$\\frac{||\\hat{\\beta}_{\\lambda}^R||_2}{||\\hat{\\beta}||_2}$",

fontsize = 15

)

The graph on the left shows how the coefficients converge as the regularisation parameter increases. For clarity, a logarithmic scale for the regularisation parameter is taken. The most prominent coefficients are highlighted in colour and line style - the data are standardised, so the scale of the values does not matter;

The vergence is plotted to the right on the ordinate:

Where:

\(||\beta||_2 = \sqrt{\sum_{j=1}^p \beta^2_j}\) - is the Euclidean distance of the coefficients \(\beta\) from the origin;

\(\hat{\beta}\) - coefficients obtained by the least squares method (equivalent to the coefficients obtained at \(\lambda = 0\));

\(\hat{\beta}^R_{\lambda}\) - coefficients obtained using regularisation.